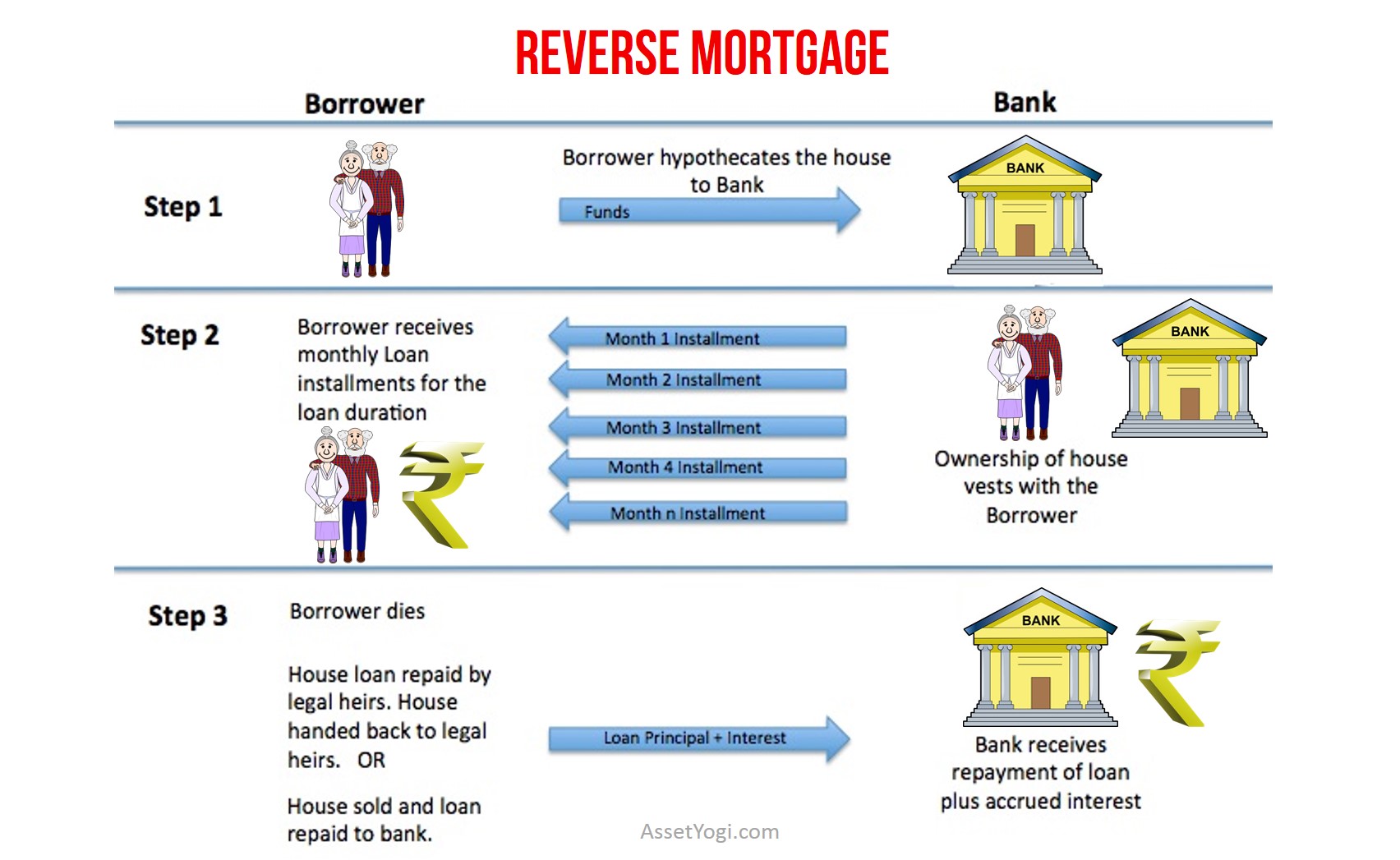

Prominent independent organization that gives objective pointers out of money possibilities, house safety so you can handling the techniques.

Offering a house isnt a quick and easy activity. Rationally speaking, it will require up to five months or maybe more to achieve this. Just what happens if you discover your ideal household during the a affordable cost, but they are struggling to finish the sales of your own existing assets in the long run? Here’s in which connecting fund help! In this article, we are going to take you from the means of bringing a link loan, as well as respond to several of the most asked inquiries.

1. Capitalised Notice Connecting Mortgage

Not as much as which bridging financing, the entire cost of the new domestic would-be covered by the new bridging mortgage. You will avoid paying for each other your existing house’s home loan and you may new connecting mortgage, while the payments towards capitalised attract connecting loan merely starts just after the fresh income of your own established property. The eye you accrue would-be put into their principal count, and you can need to make a lump sum from the amount at the conclusion of the mortgage term.

This is best for those who don’t want to grab into heavy economic weight out-of controlling both costs within same big date cash loan Derby Connecticut.

2. Simultaneous Installment Connecting Mortgage

The fresh new parallel repayment connecting mortgage ‘s the complete opposite away from a capitalised attract bridging financing. Significantly less than it loan design, you would need to pay the principal and you will focus commission concurrently on the loan term. Naturally, you may face higher quantities of economic load. not, and also this implies that might will enjoy straight down attract fees.

Whether it still songs confusing for your requirements, don’t be concerned! From inside the Singapore, despite which bridging mortgage you choose to take, its mandated that they have to be distributed straight back contained in this half a year.

Of many Singapore banking institutions give connecting money that have differing packages. Instance, DBS’s connecting loan is actually labelled on the DBS Best Rate, currently updates from the 4.25% p.an effective.. At the same time, there is no secure-when you look at the period. Important Chartered’s HDB bridging mortgage is pegged towards the 3-week SORA rate + dos.50% p.a good.. It, yet not, only relates to HDB assets.

You’ll be able to submit an application for bridging finance regarding subscribed money lenders. A full a number of licensed currency loan providers is available here . The eye pricing licensed currency lenders fees try capped at cuatro% p.good.. Signed up currency loan providers normally have reduced stringent qualification criteria, making it the best choice for specific.

That is qualified to receive a bridging financing?

Singapore People and you can Permanent Residents over the chronilogical age of 21 years old meet the criteria to apply for a connecting mortgage. The fresh bridging loan amount you could potentially located depends on the fresh new CPF likely to feel returned otherwise requested bucks proceeds from the newest revenue of the newest assets. The bridging mortgage covers the bill number you require beyond the new LTV limit. The current LTV limitation lay by MAS to have loans try 75%, since LTV maximum having HDB fund try 80%.

Consequently you’ll be able to to help you acquire to 24% of your own price for your this new property. For-instance, if the new assets costs S$one million, therefore the LTV limitation was 75%, the lending company will simply give you all in all, S$750,000. The remaining S$240,000 (24%) might be covered by the fresh connecting financing. The lending company will not be able so you’re able to bridge the first 1% deposit that you’re going to must have no less than to place a solution to Purchase.

How do i make an application for a bridging financing?

Making an application for a connecting financing is fairly way more quick than applying for virtually any financing. The procedure is only going to elevates a few days and will be also finished in day. Generally, all of the banking companies follow comparable strategies, but make sure to do your homework just before committing to one to, because there may be certain requirements mandated by the certain finance companies.

And the application form, files that need to be recorded are very different with regards to the possessions method of. Should your current property is an HDB, you will need to submit the most recent CPF detachment statement, solution to buy into the existing possessions, account declaration from your established bank/HDB proving the loan equilibrium, and some emails from HDB, because of the caveat lodged to your present assets.

In case your current home is a personal possessions, you have to submit the new properly worked out solution to purchase and latest CPF detachment report to suit your present property, membership statement exhibiting their current mortgage harmony, get it done page throughout the buyer’s attorney, and the caveat lodged with the existing possessions.

Any kind of most charges appropriate to me?

Fundamentally, you’re not subject to people processing costs, or pre-fee and termination costs, no matter if this may differ from financial to help you financial. There may not, become additional legal fees implemented by your attorney. A standard payment away from dos% towards the overdue number is energized as well as typical interest for people who default on the financing. At the same time, later fee fees anywhere between 3% so you can 5% can also implement, based on your chosen lender.

Develop that notion of a bridging mortgage feels quicker international to you. If you opt to take on a connecting loan out-of an effective financial, an authorized money-lender, or perhaps not take it whatsoever, definitely perform a whole lot more browse and you may seek qualified advice prior to investing in anything whatsoever, this might be an enormous-admission buy!