Divorce proceedings or perhaps the end out of a love is a difficult and psychological day, specially when you are considering common property eg a combined mortgage. For folks who along with your ex lover-mate features a shared financial together, you elizabeth in the home loan. Regardless if you are looking to spend less, to store the house or property, sell otherwise refinance it, there are things you can do to eliminate your ex away from the combined mortgage. Within article, we’ll walk you through the entire process of deleting an ex of a mutual mortgage, like the reasons for having doing so, the potential can cost you, additionally the steps working in rendering it alter.

What’s a combined financial?

A joint home loan is home financing one two or more anybody take-out to one another to shop for property. From inside the a mutual financial, all activities are just as accountable for paying the loan, regardless of what much each person resulted in this new deposit otherwise the way the possessions ownership was split up. Shared mortgages are common certainly one of ily members, otherwise family and friends representative whom decide to inhabit the fresh new assets to one another.

As to the reasons treat an ex lover away from a combined home loan?

You can find reasons why people regarding a mortgage together may must treat their ex out of a mutual financial. These may is:

- Matchmaking dysfunction: If the several distinguishes otherwise gets separated, one party may want to reduce its ex lover from the joint home loan to help you sever economic ties and move on with the life.

- Monetary disagreements: If a person class is not maintaining its mortgage repayments or is and make economic behavior that other people disagrees that have, the other people may want to remove them on mortgage to eliminate one bad influence on their credit rating otherwise economic problem.

- To invest in a separate property: If one cluster would like to pick an alternative possessions, they might have to lose its ex lover regarding shared mortgage to be entitled to an alternative mortgage.

- Refinancing: If one people desires to re-finance its present home loan, they might need treat the ex from the combined mortgage in order to get it done.

Points to consider before deleting a name regarding a mortgage:

Before making a decision to eradicate an ex from a combined mortgage, you should look at the financial implications. This involves understanding the potential will cost you and you will dangers active in the process. A few of the key factors to remember were:

- Refinancing will set you back: If you are planning to get rid of your own ex’s title regarding the mortgage by the refinancing the mortgage, make an effort to think about the will set you back in it. Refinancing normally comes to charge such as for example appraisal will cost you, identity insurance policies, and bank charges. It is important to see this type of will set you back upfront and you can foundation all of them to your your decision-and come up with techniques.

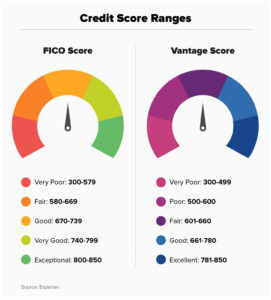

- Credit history perception: Deleting your ex’s name from a combined mortgage could potentially feeling your credit score. If the ex lover features good credit, the label with the financial was permitting their borrowing get. Removing its name you could end up a decline on your own credit rating, specifically if you have an enormous the balance towards the home loan.

- Security delivery: When removing an ex off a combined home loan, you will have to consider tips split new security throughout the assets. It is a complex techniques, particularly if you have made high home loan repayments and your ex lover possess contributed nothing otherwise absolutely nothing. You will have to try using a reasonable delivery of the equity and discover if you need to cover an attorney otherwise mediator to help with the process.

- Rates of interest: While you are removing your ex’s name from the mortgage by the refinancing, it is very important look at the newest rates of interest. If the pricing have increased because you first got from the mortgage, you may want to end up getting a top interest rate, that’ll end up in highest monthly obligations.

Judge requirements when planning on taking a name off of the financial:

In the united kingdom, deleting a reputation away from a joint home loan requires the arrangement off both parties involved in the mortgage price. You can find judge and you can financial factors to consider before proceeding on treatment.

First of all, the loan bank has to be advised regarding personal circumstances and you may the latest purpose to get rid payday loans Lexington of a name from the financial. They’ve their rules and functions that have to be observed, and they will need commit to the change into the possession. The lender tend to gauge the leftover borrower’s financial situation to make certain that they are nevertheless able to spend the money for mortgage payments into their.

It is very important note that the remaining debtor e, which is susceptible to the financial institution home loan broker’s common affordability and you may borrowing monitors. The lender also look at the collateral about assets and you can need an effective valuation to get accomplished.

From an appropriate direction, getting rid of a reputation away from a mutual financial may need a legal import off control that occurs. This may cover the conclusion regarding an exchange out-of Guarantee file, which is a legally joining arrangement that transmits possession of property of mutual brands to one term. The fresh new import sufficient equity will need to be registered for the House Registry, that will take many weeks.

It is best to look for legal services ahead of proceeding towards the elimination of a name out of a mutual financial. A solicitor can deal with the fresh new legal procedure and ensure that all the requisite paperwork is accomplished accurately.