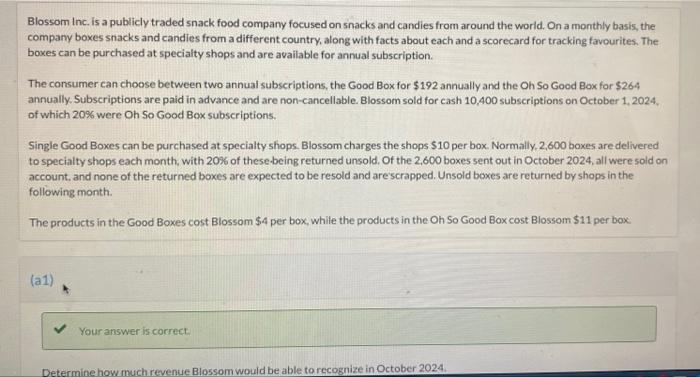

If you find yourself purchasing your very first family, you can also be hearing essential mortgage conditions into basic day. Before you apply having a mortgage, its crucial you have an obvious comprehension of exactly what the words imply and just how it impact the homebuying experience. Start with looking at one particular misunderstood words inside our infographic less than and you will consult with a mortgage expert to have advice.

While you are perplexed by the following the conditions, you aren’t by yourself; they might be some of the most misinterpreted financial terminology. Also some of the most crucial, very guarantee that you may be certain of next definitions.

The procedure of making typical monthly obligations one reduce your home loan over time. Such as for instance, if you take away a 30-year home loan, your loan is totally amortized once you’ve produced 360 month-to-month costs.

Note: A keen amortization plan helps guide you a lot of for every single commission happens in order to dominating and you can desire. Because you reduce the mortgage, a lot more of their commission is certainly going to prominent much less in order to focus.

The last action of your own homebuying procedure. Closing costs is fees for expenses required to complete-or personal-your financial. They are possessions taxation, appraisal fee, origination percentage/products, software commission, credit file percentage, conceptual up-date otherwise term lookup commission, bank term insurance coverage payment, lender attorney fee, and you can probably far more.

Your credit report is actually a record of your borrowing and fee affairs, instance if you have paid back their costs towards the schedule plus complete.

Your credit score are lots you to definitely positions exactly how most likely you should be generate mortgage money promptly based on the guidance on your own credit file.

Tip: You can access your credit report anytime at no cost having Community Bank’s Borrowing from the bank Mate SM provider. Have the facts from the cbna/digital-banking/credit-lover

Measures up your debt on money. Your estimate it from the totaling your own month-to-month obligations costs and you can loans and also the will cost you of your new home loan (dominating, focus, fees, and insurance policies) and you can splitting one to by the terrible monthly income, that is your pay ahead of taxation and write-offs try removed.

Whenever reviewing the financial app, their lender will during the DTI to evaluate whether you will end up in a position to carry out brand new monthly obligations.

The quantity you only pay in advance when selecting a house, constantly indicated just like the a portion of one’s house’s worthy of. Then you certainly take-out a mortgage to expend the others more date. For example, for folks who place 20% upon good $300,000 house, your deposit will be $sixty,000 plus home loan would be $240,000.

Tip: If at all possible, its worth waiting if you do not is also lay 20% down, so that you need not shell out PMI that will rating a straight down interest rate.

Such as for instance, if your gross month-to-month earnings try $six,000 each day you pay $2 hundred toward a student loan, $3 hundred on an auto loan, and $1,000 on the home loan, your month-to-month loans repayments would-be $step one,five hundred plus DTI would be twenty five% ($1,five hundred try twenty-five% away from $6,000)

The brand new percentage of your house which you own. With each mortgage repayment you create, you make security, managing much more owing the lending company faster. To help you calculate your own security, merely subtract extent you owe on your household from the market value.

When you purchase a house, your own lender will get put up an enthusiastic escrow membership to pay for the assets taxes and you can homeowner’s insurance policies. After closure, they’ll place a portion of for each month-to-month mortgage repayment into the escrow membership and will pay your fees and insurance coverage once they was owed in your stead.

The interest rate to the a fixed-rates mortgage is actually secured during the and does not changes within the term. Conversely, the rate towards the a supply can fluctuate with industry conditions after a first introductory months. Meaning their payment per month can go up otherwise off while the really, although not more than the new loan’s interest limits, do you know the extremely a speeds can increase during the per year, or higher living of your title.

Tip: When the interest rates shed, your monthly obligations on the a supply could go off also, that makes Possession a fascinating alternative when prices try highest. In case rates rise loans in Kensington, your repayments is certainly going right up. Make certain you has push space on your own funds when you’re provided an arm.

Their interest rate is a percentage of your financial you have to pay each year as cost of credit the bucks, excluding charge. However the Annual percentage rate is actually a more useful matter since it boasts the latest related charges, for example issues and closing costs.

The fresh LTV measures up the loan total the residence’s current ple, by taking aside an excellent $2 hundred,000 financial on the property assessed at $two hundred,000, your own LTV might possibly be 100%. But when you generate a great $20,000 deposit, your financial could well be $180,000 as well as your LTV would-be 90%. Extremely finance companies wanted private mortgage insurance coverage when you fund more 80% LTV but at the People Financial you can prevent spending PMI costs with just ten% down.

However, from the Society Financial you might avoid spending PMI will cost you that have only ten% off

When a lender provides you with an instant guess of your financial matter you will probably qualify for according to a basic report on your finances. The lending company will look at your credit score and ask for records confirming your income, property, and you will expense. If you’re prequalified, you’re getting good prequalification letter to your cost of the house you will want to look for. Following, once you create an offer for the a house, your application is certainly going from the lender’s underwriting technique to prove everything ahead of offering finally acceptance.

The amount of the loan your acquire. Desire is really what the lending company charge you to have borrowing the money. Your own monthly payments see each other dominant and you may appeal, and also as you only pay down the principal additionally pay reduced notice towards down remaining mortgage amount.

Extremely banks wanted personal mortgage insurance rates after you financing over 80% LTV to protect the providers up against loss if you can’t create repayments. The PMI premium is typically added to your monthly home loan bill, and once you have based a lot of collateral on your own domestic you should be able to terminate PMI.

When a mortgage underwriter verifies your income, debt, property, credit history, and you will factual statements about the property you may be to get to decide just how much regarding a threat its to help you mortgage the currency, and in the end assist their bank select whether to agree the loan.