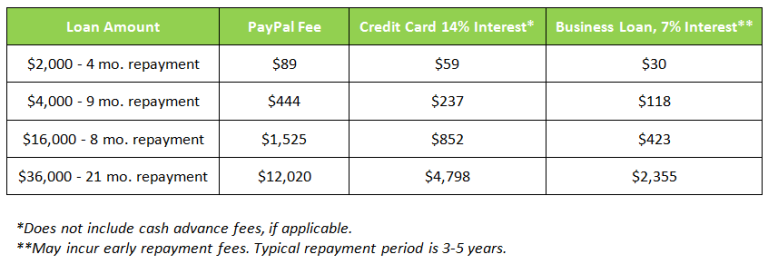

Just how much Put Manage I need To own A home loan?

Exactly how much put create I need for a https://paydayloancolorado.net/starkville/ mortgage? This is a common matter I’m requested, and also in small, there is absolutely no decisive answer – it’s up to you. It comes down to the money you owe as well as how much charge and you may appeal you’re ready to shell out discover onto the housing marketplace.

Reworking so it picture to help us work out just what put we you prefer, the new picture will get D = P + C – L – G

- You’ve discover a beneficial tool when you look at the Perth that you want to purchase plus the purchase price is $430,000.

- WA Stamp responsibility towards purchase are $fourteen,440.

- You will be pregnant a deeper $3000 within the pick will cost you such as for example settlement costs, pest & building monitors etcetera.

- You’re not a first home buyer – so no First Home Owner’s grant or reduced rate of Stamp Duty.

Option step one. 20% or maybe more of your own purchase price + get costs. This really is the fresh phenomenal contour in home credit. Lots of lenders throughout the Australian household lending field usually provide up to 80% of cost otherwise worth of (lenders tend to give from the lower of these two beliefs if it differ) in place of asking Lenders Financial Insurance rates (LMI). If you have a good 20% deposit + will set you back, then you are in operation. If you’re mind-employed and you do not have the full selection of documentation (lowest doctor), next lenders fundamentally want more substantial deposit.

Therefore in our condition more than, we know the lending company often provide doing $344,000 (80% regarding $430,000) in place of billing LMI (if in case we fulfill each one of other credit criteria).

Simply how much Put Do I wanted Having A mortgage?

Alternative dos. 5% – 20% of purchase price + get costs. If you cannot help save 20%, never stress. Most Australian loan providers will nonetheless give to 95% of the property worth, nonetheless will charge you Lenders Home loan Insurance.